A consumer manufacturer’s marketing director wakes up one Tuesday with a one-point margin lift opportunity. The category data says it. The internal benchmark says it. The sensitivity analysis says it. By the time the proposal reaches the CFO it has been diluted by twelve emails, three sales objections, two distributor pushbacks, and a brand manager who is worried about volume. The proposal goes back into the queue. Twelve weeks later the marketing director is in the same office, looking at the same slide, having the same conversation. The one-point lift is still real. The decision to take it has not been made.

In This Article

This is the failure pattern I have seen at every consumer business with a margin opportunity it does not capture. The math is right, the analysis is right, the seniority of the people in the room is right. What is missing is the structural mechanism that converts an analytic opportunity into a price-change decision, and the discipline that holds the decision in place against the predictable objections that follow it. The mechanism is the pricing committee. The discipline is its operating model. This article is the architecture of the committee that worked in production, and the operating cadence that turned a 1-point margin lift from an analytic finding into a recurring P&L item.

The companion article How a 1-Point Price Increase Becomes a Real Project covers the analytic side: how you identify the 1pp opportunity, how you size it, how you ladder the levers. This article is the governance side: who is in the room, who reports to whom, what the room actually decides, and why the decision does not unwind in the six weeks after it gets made. The two articles are halves of the same project. The analysis without the governance produces a slide that does not become a price change. The governance without the analysis produces a committee that meets monthly and changes nothing. Both, together, produce a margin lift that recurs.

The deliverable from a fractional CDO engagement on a pricing program is a five-person standing committee, an eight-tool tracking dashboard, a four-lever execution playbook, and a 12-page pricing order document that codifies how price changes get proposed, reviewed, approved, and rolled out. The remainder of this article is each of those four pieces in turn.

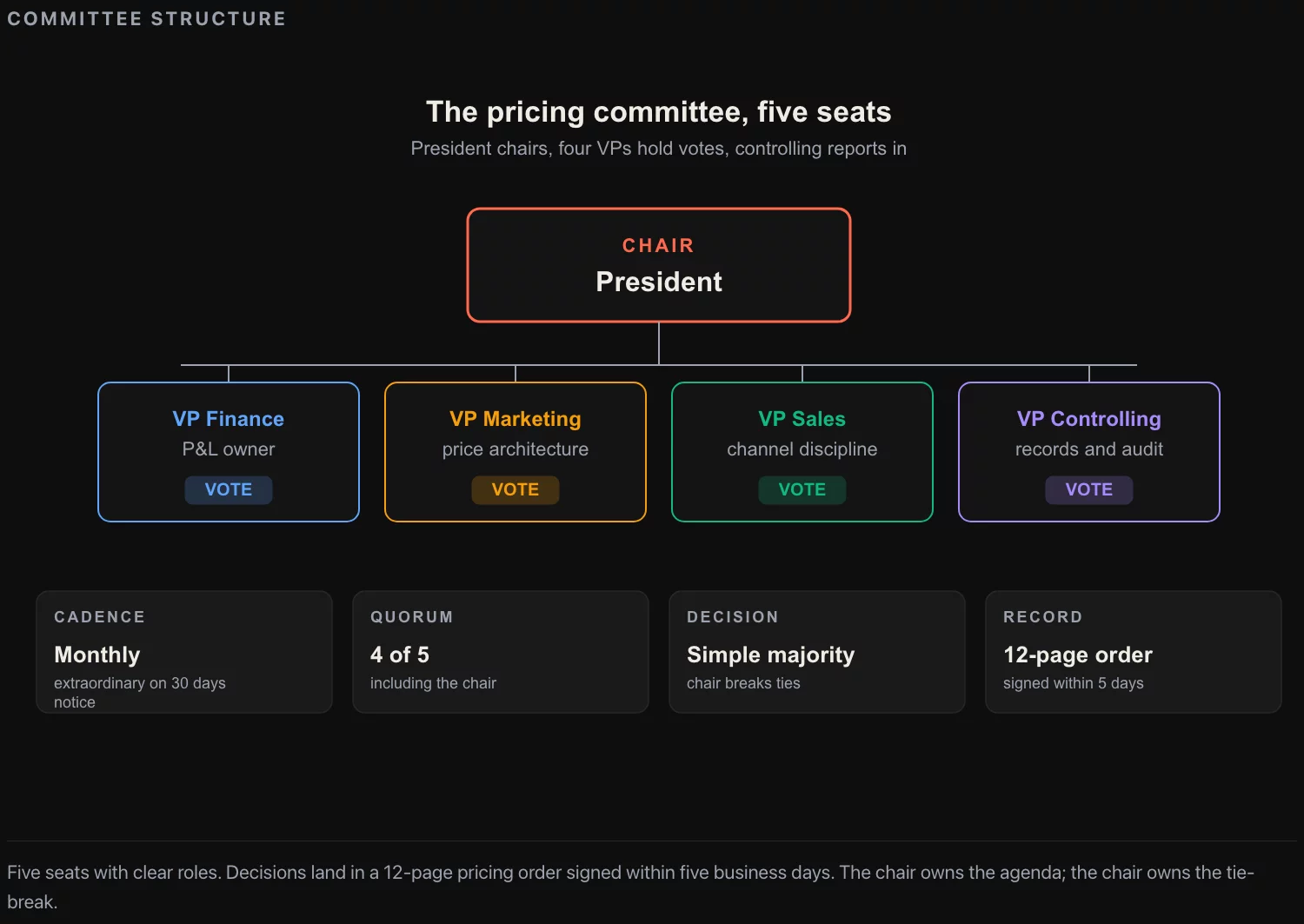

Who is actually in the room

The committee is five seats. The composition is non-negotiable: each seat exists because the seat next to it would not give them the answer they need without it.

VP Finance. The Finance VP owns the P&L impact of every price change. The role of Finance in the room is to be the keeper of the profit-pool math: every proposal arrives at the committee with a six-month and twelve-month revenue impact, a margin impact, a volume sensitivity, and a working-capital footprint, and Finance is the seat that signs off on the math before the committee votes. Finance is also the seat that authorizes the trade-spend reallocations that fund some price moves, which is the place where most pricing programs quietly fail.

VP Marketing. Marketing is the seat that proposes most price changes. The marketing organization owns the brand positioning, the consumer-price research, and the category-share strategy, all of which produce the analytic findings that surface as pricing proposals. Marketing presents the proposal, defends the analytic basis, and owns the brand-side execution after approval. In the source structure I built this against, the pricing manager who actually staffs the proposal sat inside marketing; this is the right organizational placement for most consumer businesses because the proposal is brand-centric and the marketing team has the consumer-research budget.

VP Sales. Sales is the seat that owns the customer-facing rollout and is the source of most realistic objections to a proposed price change. The sales VP knows which key accounts will retaliate, which distributors will pass through the increase versus absorb it, which channels will substitute toward private-label, and what the rollout cadence has to look like to avoid a volume shock. Without sales in the room, the proposal is analytically sound and operationally naive, and the rollout is what kills it in the field. With sales in the room, the operational concerns are surfaced before the decision is made and either addressed in the proposal or accepted by the chair as costs of the lift.

Controlling (head of FP&A or category P&L), reporting in. Controlling is not technically a VP in most structures, but the head of category P&L or the head of FP&A reports into the committee with the calculation of revenue and profit-pool impact for every proposal. This seat is the one that holds the committee accountable to the calibration log: the previous quarter’s price changes are tracked against their forecast revenue impact, and the variance is reported at every meeting. Controlling is the part of the committee that makes the committee a learning body rather than a decision body.

Five seats. Each one decides; the chair breaks ties. The committee meets monthly on a fixed cadence and the agenda is preset. Anything that needs more than a one-hour discussion gets bumped to a working session before the next month.

What the committee actually decides

The committee runs on three deliverables per cycle. Each deliverable has a single owner, a single approval path, and a documented set of inputs.

The first deliverable is the annual price increase schedule. Once a year, typically in the fall planning cycle, the committee approves a schedule of base-price changes for the upcoming twelve months. The schedule is per-brand, per-SKU, per-channel where the granularity matters. The schedule is not an aspiration; it is a commitment, with execution dates inside the next twelve months, that drives the financial plan. The schedule is owned by Marketing and proposed at the September meeting; it is reviewed by Finance and Sales in the October meeting and approved at the November meeting in time for the financial plan to be finalized.

The second deliverable is the in-year base-price-change proposal. Between scheduled changes, the committee can authorize off-schedule base-price changes in response to category dynamics: a competitor price move, a regulatory change, a meaningful shift in input costs, a category mix shift that opens up margin in one tier. Off-schedule proposals require additional substantiation: the analytic basis from Marketing, the revenue and margin model from Controlling, the rollout plan from Sales, the channel impact from the sales VP. The committee approves or declines at its monthly meeting. The decision is documented in the pricing order and published to the affected teams within five business days.

The third deliverable is the new-product price approval. Every new product launch that has a meaningful share of category revenue (typically anything above 1% of total category sales at launch) goes through the committee for initial pricing approval, positioning relative to the existing portfolio, and the first-six-months trajectory plan. New-product pricing is the deliverable that breaks most committees, because new product launches are time-pressured and the committee cadence is monthly; the fix is to set a clear threshold below which the brand team approves pricing on its own, and only the launches above the threshold come to the committee.

Three deliverables. Twelve meetings a year. A documented agenda. A decision log that the next meeting reviews. The committee that runs on this cadence captures the 1-point margin lift; the committee that runs on a different cadence does not.

The four levers the committee operates

The McKinsey diagnostic that informed my approach to this work identified four levers that together produce a 1-point realistic price lift in most consumer categories. The committee’s job is to ladder these four levers across the calendar in a way that protects the brand and produces the lift.

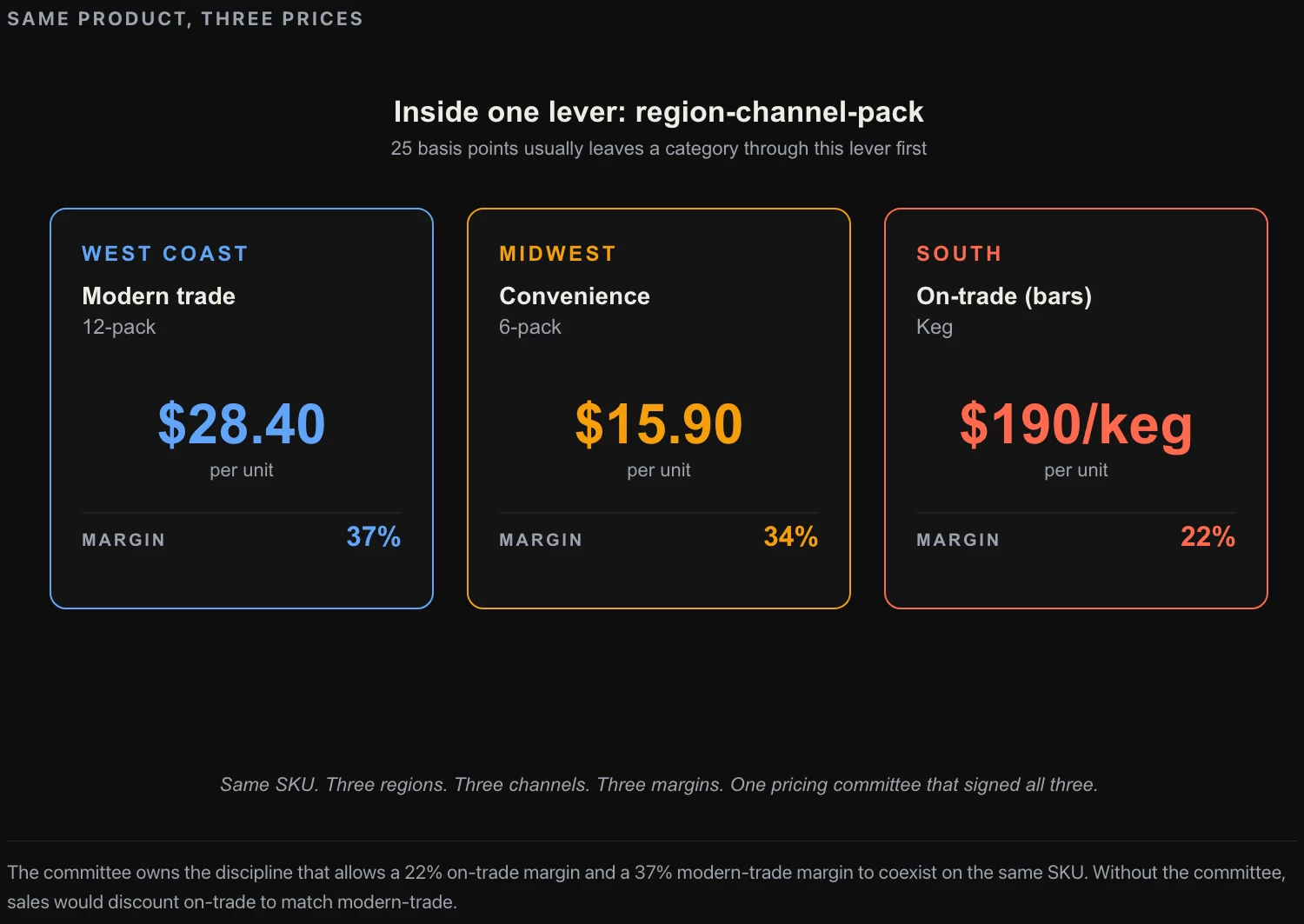

Region-channel-pack pricing (RCPP). The granular pricing decision is whether specific regions, specific channels, and specific pack sizes are priced optimally relative to one another. This is the lever where most consumer companies have the largest hidden opportunity, because the granular pricing has typically been set by historical accident and has drifted from the optimum over years. A region-channel-pack pricing study identifies the 10% to 20% of SKU-region-channel combinations where current pricing is more than 5% below the optimum, and the lift is captured by gradually raising those combinations toward the optimum. In a typical consumer category, RCPP contributes 25% to 35% of the 1-point lift opportunity.

Distributor pricing. The distributor-pricing decision is the structure of discounts, bonuses, and rebates that flow from the manufacturer to the distributor and downstream. This is the lever where most manufacturers have meaningful value leakage: discounts that were granted in negotiation years ago and were never recovered, bonus structures that incentivize behavior the company no longer wants, rebate categories that are no longer aligned with the strategy. A distributor-pricing review identifies the 5% to 15% of distributor agreements that are creating value leakage, and the lift is captured by renegotiating those agreements on their next renewal cycle. In a typical consumer category, distributor pricing contributes 15% to 25% of the 1-point lift opportunity.

Pricing process and organization. The process lever is the structural improvement to who, when, and how price decisions get made. This is the lever the committee itself is the embodiment of. It includes the committee charter, the agenda structure, the tracking-tool dashboard, the documentation of decisions, the calibration log, and the cadence of the committee. The process lever does not produce a one-time lift; it produces the conditions under which the other three levers keep producing lift in subsequent years. In a typical consumer category, process contributes 10% to 15% of the 1-point lift opportunity in the year you build it, and is the precondition for sustaining the other 85% to 90% in subsequent years.

Four levers, summing to the 1-point lift. The committee does not work all four levers in the same quarter; it works them in sequence over twelve to twenty-four months, with a deliberate cadence that respects the operational reality of each lever.

The eight tools the committee runs on

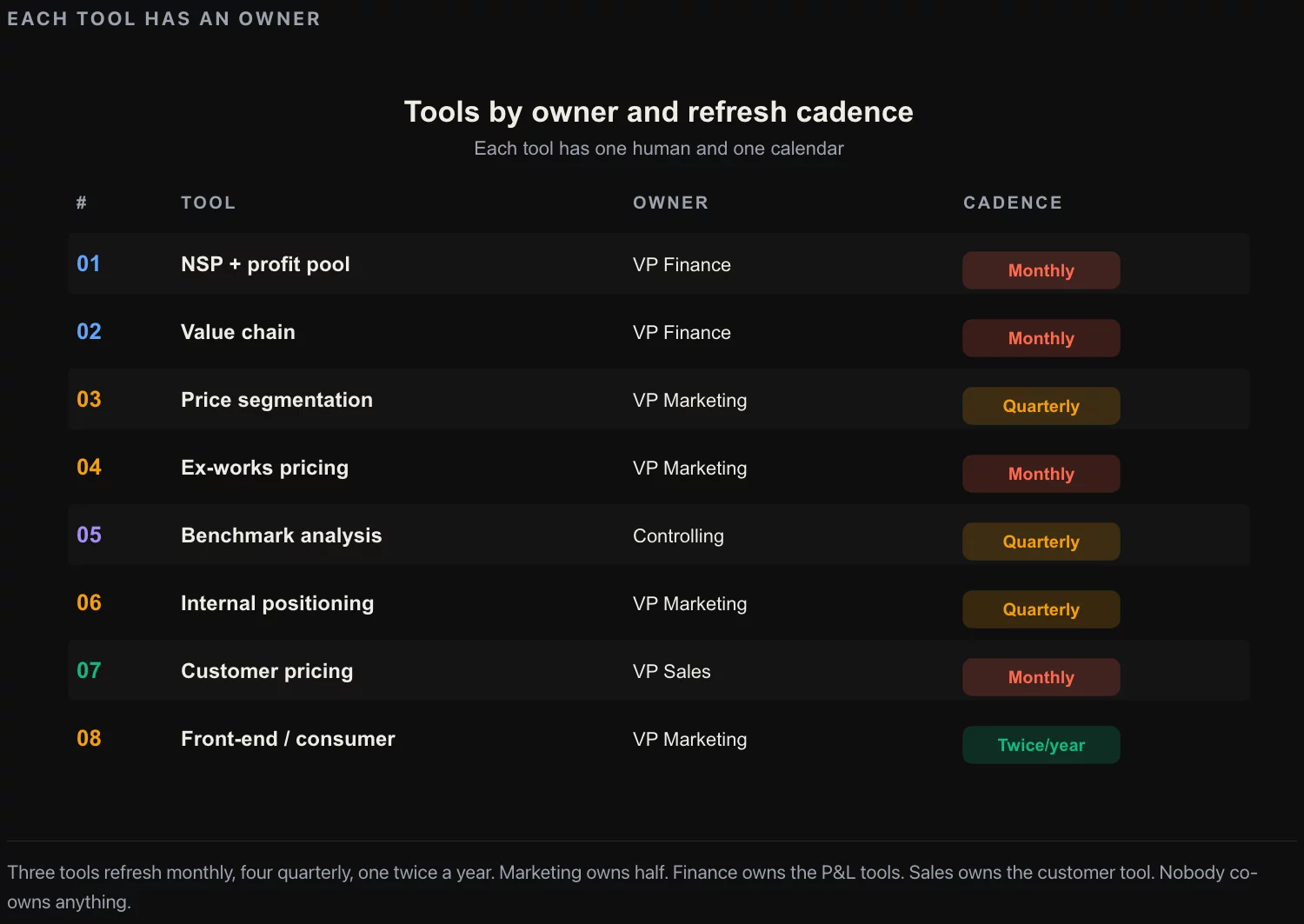

The committee’s monthly agenda is fed by eight tracking tools. Each one is a dashboard or analysis that updates monthly or quarterly and feeds the committee’s decisions.

Value chain analysis. The flow of value from manufacturer to consumer: manufacturer NSP, distributor mark-up, retailer mark-up, consumer price, with the share captured by each link. This is the tool that surfaces value leakage and identifies the distributor and retailer mark-up arbitrage opportunities. Updated quarterly. Owned by Marketing.

Price segmentation analysis. The distribution of SKU prices across consumer tiers: economy, mid, premium. Surfaces the tier-mix shifts that drive category margin and the gaps in the portfolio where a new tier-positioned SKU could be priced into the white space. Updated quarterly. Owned by Marketing.

Ex-works price. The manufacturer’s selling price before transport, distribution, and channel mark-ups. The cleanest comparison across regions and channels. Updated monthly. Owned by Controlling.

Benchmark analysis. The competitive set’s pricing on equivalent SKUs across the categories the company plays in. Sourced from retail-audit data where available and from public retail prices where panel data is not affordable (the public-data methodology lives in Market Sizing Without a Nielsen Subscription). Updated monthly for top SKUs, quarterly for the full set. Owned by Marketing.

Internal brand positioning. The pricing of the company’s own brands relative to one another within the portfolio. Surfaces cannibalization risks (premium brand priced too close to mid-tier, eroding the mid-tier) and white-space opportunities (gap between premium and super-premium that could support a new SKU). Updated quarterly. Owned by Marketing.

Customer pricing and mark-up management. The list of agreements with key accounts: list price, agreed discount, performance bonus structure, payment terms. Surfaces the agreements that are creating value leakage and the agreements where the renewal cycle is approaching. Updated monthly. Owned by Sales.

Sensitivity, thresholds, front-end price, and consumer price research. Four related tools that together quantify the consumer response to a price change at the SKU level. Sensitivity is the elasticity estimate. Thresholds are the psychological price points (e.g., the SKU that is currently priced at $4.99 and faces a different elasticity above $5.00 than below it). Front-end price is the shelf price the consumer sees, which depends on retailer mark-up and is not the same as the manufacturer’s list price. Consumer price research is the CBC (choice-based conjoint) or BPTO (brand-price trade-off) study output that produces the elasticity estimate. Updated annually for the elasticity model, monthly for the front-end-price tracking. Owned by Marketing.

Eight tools. Each one feeds a specific decision. The committee’s monthly meeting opens with the dashboard of the eight, reads the changes against the previous month, and uses the changes to identify the next month’s proposed price moves.

Three patterns to never let the committee accept

Three failure patterns in pricing-committee operation that compound over the course of a year. The committee chair’s job is to refuse each one when it surfaces.

The seasonal-price-promotion-as-strategy pattern. A brand team proposes a Q4 promotional discount that is intended to drive volume during the holiday quarter, and frames it as a “strategic positioning move” rather than a tactical promotion. The committee approves it because the proposal looks strategic. The discount lands, drives the volume, gets baked into the customer’s reference price, and the following year the same brand cannot raise the list price by 2% because customers are now anchored to the promotional price. The pattern is recognizable by the proposal that uses the word “strategic” three or more times without naming the specific structural change the discount is supposed to produce. The committee should reject any promotional discount that does not have a documented exit plan.

The keep-up-with-the-competition pattern. A competitor lowers prices on a key SKU; the brand team proposes a matching price reduction “to protect share.” The committee approves the matching reduction. The reduction lands, the share is protected, the margin contracts, the competitor follows the matching reduction with another reduction, and the brand team comes back next quarter with another matching proposal. The pattern is the price war the committee did not realize it was entering. The committee should require, before approving any reactive price reduction, an analysis of whether the competitor’s pricing is sustainable for the competitor and whether holding the price (with a marketing response) would be a better category outcome. In most cases the analysis is uncomfortable but the answer is to hold the price.

The trade-spend reallocation that funds the lift pattern. A pricing proposal that funds its margin lift by reallocating trade marketing spend; the committee approves it; the trade-spend reduction lands; the channel and key-account relationships deteriorate over the next six months; the share loss six months later is larger than the margin lift produced by the pricing move. The pattern is the false economy of funding a pricing lift with a trade-spend reduction that the committee assumed was non-load-bearing. The committee should require Sales sign-off on any trade-spend reduction proposed as part of a pricing move, and the Sales sign-off should reference specific accounts and specific impacts. If Sales cannot name the impact, the trade spend in question was load-bearing in ways the analysis missed.

Three patterns. Each one is rejected by a competent committee chair. A committee that approves any of them once is teaching the proposing teams that the pattern works and will see more of the same in the following quarter.

Calibration: how you know the committee is working

The pricing committee earns the right to keep operating only if the price moves it approves match the financial impact it forecast at approval time. The calibration log is the tool. Every approved price change carries a six-month and twelve-month revenue and margin impact forecast at the time of approval; the actual six-month and twelve-month impact is computed and logged at the corresponding milestone; the variance is reviewed at the meeting following each milestone.

The variance is rarely zero. The discipline is to name the variance, decide what it teaches the committee about the model, and update the next price-change proposal’s analytic basis accordingly. A committee that produces variances of less than 5% on six-month forecasts is a committee whose pricing model is well calibrated. A committee that produces variances of more than 20% is a committee whose model is broken; the next quarter’s work is rebuilding the elasticity model, not approving the next price change.

The calibration log lives in the same document as the agenda. It is reviewed at the start of every meeting. Past decisions are visible. The pattern of misses is the input to the next decision. A committee without a calibration log is a committee that is making the same mistake every quarter and not noticing.

What to do this week

If you are running a consumer business with a category-margin opportunity you have not captured, three actions before next Tuesday.

Pull the org chart for the team that is currently making price decisions. If pricing decisions are being made in the seam between brand marketing and category sales without a documented committee, the structural mechanism is missing and the next quarter’s work is building it. The committee charter is a one-page document; drafting it is two hours. Getting the five people in the room is the harder part.

Pick the brand in your portfolio with the highest historical margin variance month-to-month. Pull the last twelve months of average net selling price by region and channel. If the variance across regions is more than 8% for the same SKU, the region-channel-pack pricing lever has unrealized opportunity in your category, and the next quarter’s first analytic deliverable is the RCPP gap analysis. The 8% threshold is empirical; in most consumer categories the gap is between 5% and 12% and the upper half of the range is consistently underpriced regions.

Ask the head of FP&A for the calibration log on the last three price changes the company made. If a log does not exist, the next quarter’s deliverable is the log, not the next price change. A pricing program without a calibration log is a pricing program that cannot learn from its own decisions, and the 1-point margin lift will be diluted into noise within twelve months of the first move.

Three actions, two afternoons. They do not produce the committee. They produce the diagnostic that tells you which of the four levers is most starved for governance in your specific business. The committee is the structural mechanism that converts the diagnostic into a recurring P&L item. The diagnostic is the part the brand and sales teams can do on their own in the next two weeks. The committee is the part the CEO has to sponsor.

![[REVIEW] Looker Studio vs Power BI 2026](https://valiotti.com/wp-content/uploads/2026/06/looker-studio-vs-power-bi-2026-hero-768x512.png)